Home > Insurance Blog > Tree damage claim complexities

A tornado outbreak on Easter Sunday 2020 left 33 people dead, making it the deadliest in over six years. Tree damage tends to be one of the leading causes of fatalities in tornados, hurricanes, or severe thunderstorms. Along with the threat to life, falling trees often cause property damage. Whether it is a flying branch that smashes through a window or the upper portion of a tree’s trunk falling on a roof, trees become dangerous projectiles during a powerful storm. It is important to understand tree damage claims and how they can be challenging for adjusters and homeowners alike.

Tree damage and insurance coverage

Home damage may vary significantly based on the weight of a tree, how much of the tree falls on a home, and where on a home the tree makes contact. For example, if an entire tree falls on a home, then the roof damage will likely be significant. On the other hand, if a tree limb falls on the roof or strikes the side of a house, then generally the damage will be less significant. Additional complexities arise if the tree punctures the home and creates an opening for rain or wind to enter. The length of time required for home repairs caused by tree damage will also depend on these variables. Significant tree damage will take much longer to repair than minor damage alone. Following tree damage to a property, determining insurance coverage is often a challenging task. If a healthy tree falls in a covered event, such as a thunderstorm, then the insurer will most likely cover the home damage. If however, a tree is diseased, unhealthy, or dead and falls causing damage to a home, the insurer may not cover the related damage.

Confusion often arises when a tree on a neighbor’s property falls and damages a homeowner’s property. When this occurs, homeowner’s instinctively think that the neighbor is responsible for the damage to their property since it was the neighbor’s tree at fault. However, in most cases, even if a tree is not located on a homeowner’s property, if it damages their home, then the homeowner’s policy should respond. Another factor affecting coverage is whether the damage was sudden and accidental. Insurers consider tree damage following a severe thunderstorm, tornado, or hurricane, as sudden and accidental. Insurers typically cover tree damage claims that are sudden and accidental. On the other hand, insurers are less likely to cover gradual tree damage. For example, home foundation damage caused by the roots of a large tree, whether on your property or your neighbors, may not have coverage.

Tree inspection and removal

Having a tree cut down and removed from a property is an expensive endeavor. As a result, if a tree falls on a property then a homeowner is very likely to try and determine if insurance will pay for its removal. In most cases, the answer is… it depends. If a healthy tree falls on a home, then the insurer will pay for its removal from the home. If, however, a large tree falls on a property but does not damage any structures, then its removal will likely not be covered by the homeowner’s insurance policy.

Homeowners must inspect trees on their property regularly. If a tree becomes diseased, damaged, or dies, then it could become an uninsured hazard to the property. Below are a few tips on how to inspect a tree.

- Start at the bottom – Observe the tree’s roots looking for any areas that may be soft or show evidence of decay.

- Closely review the collar of the tree or the area where the roots meet the trunk. Check for any missing or falling bark. Also, check for cracks in the trunk.

- Analyze the Trunk – Examine the trunk for any significant cracks or growths as these may indicate health problems.

- Observe all the way up the tree – Review the remainder of the tree looking for branches that are broken, limbs missing leaves or bark and any limbs without growth of leaves or bark altogether.

If this inspection indicates any potential problems, then the homeowner may want to have a certified arborist review the tree in order to be sure it is healthy. An arborist may also help recommend the best course of action for an unhealthy tree. Sometimes only pruning is necessary in order to help revitalize a tree.

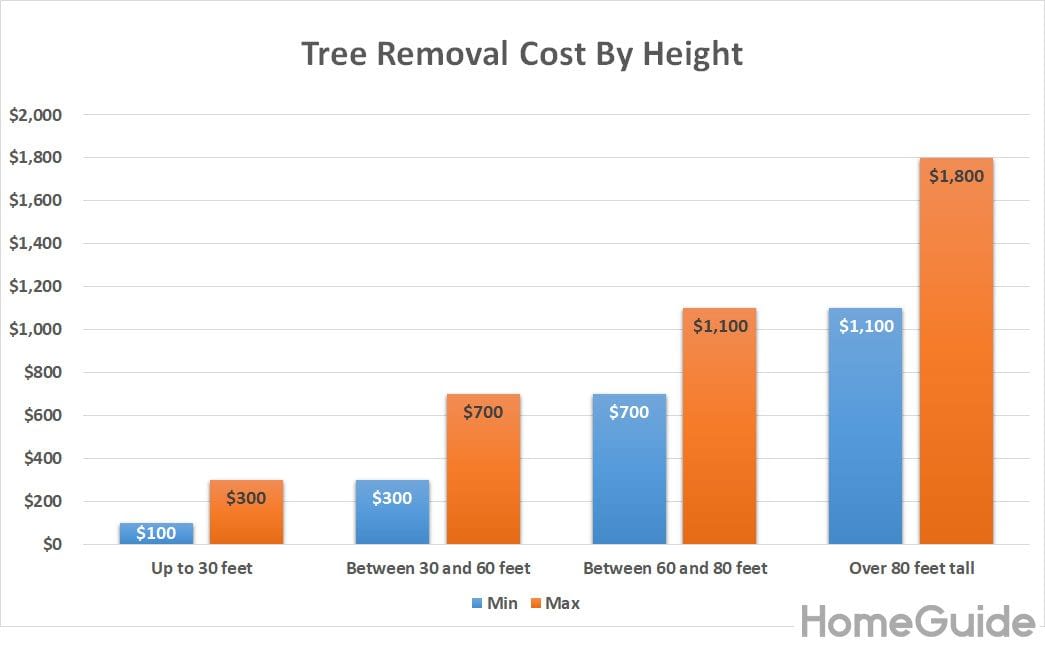

In the event that a tree requires removal, either before or after a loss, the costs can be high. Below is a list of factors that affect the cost of tree removal. Also included below is a homeguide.com chart showing the 2020 average cost to remove a tree based on its height. Immediately following a major storm, like a hurricane, tree-removal prices can skyrocket. Knowing the average cost of tree removal can help ensure homeowners do not get taken advantage of when their property has been damaged.

- The size of the tree

- The diameter of the tree

- Crown of the tree

- Weight of the tree

- Need for heavy equipment

- Wiring involvement

- Skylight involvement

- Extent of current landscaping

- Primary home or an outbuilding affected

- Is the tree embedded inside a home or building

- Number of hours the job will require

- Number of workers needed

- Type of crew

Chart Created by HomeGuide

Adjusting tree damage claims

Property adjusters face many challenges in accurately adjusting claims involving trees. Property adjusters must work closely with tree experts in order to understand the real costs involved in the tree damage. This can be especially challenging in claims with widespread damage such as tornados and hurricanes. Trees often damage the main dwelling but may end up adjacent to the structure. In addition, multiple trees may be down following a tornado or strong wind damage. These conditions make it unclear whether the tree actually caused damage or damage was due only to wind. These complexities make adjusting tree claims especially perplexing for adjusters and then homeowners as well.

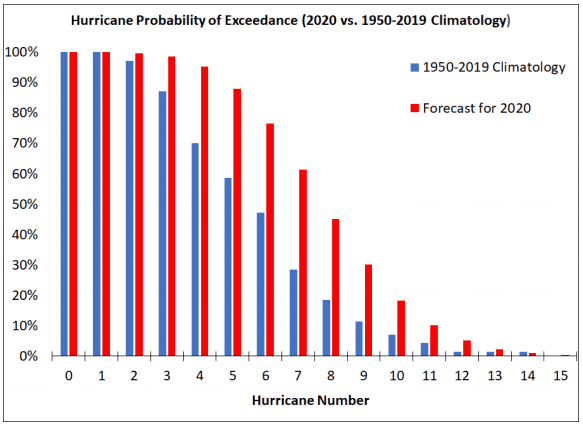

To help adjusters, insurers need to account for expected significant windstorm activity in order to accurately reserve for potential losses. Tree damage claims tend to be higher during active hurricane seasons. Based on an April 2020 report issued by the Colorado State University Department of Atmospheric Science, forecasters expect an above-average hurricane season in 2020. The below graph compares the hurricane probabilities for 2020 with the average number of hurricanes since 1950. In addition to more accurate reserves, understanding annual storm predictions help insurers adequately staff adjusters in order to tackle likely claims arising from an above-average hurricane year.

Given that meteorologists expect an active 2020 hurricane season, insurers must gear up and prepare. Likewise, now is a good time for homeowners to inspect all trees on their property. If any trees do not pass the inspection, then the homeowner needs to take action prior to hurricane season. By understanding the complexities involved in managing tree claims, adjusters can improve both their customer service skills and adjusting accuracy.