What’s driving increases in home insurance premiums?

Posted: February 1, 2022

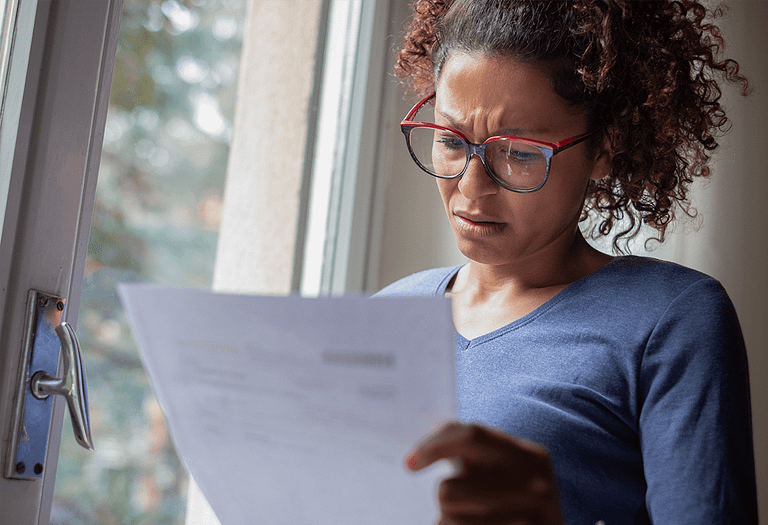

Many homeowners end up frustrated when the cost of their homeowners insurance rises. The general perception is that homeowners insurers are increasing premiums without just cause or in an effort to scam homeowners. In reality though, homeowners insurance premiums depend on several factors beyond the control of homeowners and insurers. In this article, we review these variables in order to give homeowners peace of mind...

Tips for reducing your energy bill this winter

Posted: December 9, 2021

During the winter many homeowners are surprised by high utility bills. Usually, high energy bills in the winter are a result of using your HVAC system more, but can also be attributed to holiday lights and increased usage of appliances (like your oven). Staying warm while saving energy is important if you want to be more conscious of the environment or your budget. Here are...

Holiday cooking safety tips

Posted: November 16, 2021

As we approach the holidays, we are also coming up on the time of the year when homeowners get the most use out of their kitchens. While the holidays create many safety hazards around the house, the risk of getting injured or starting a fire is especially high in the kitchen. Here are a few of our best holiday cooking safety tips to help you...

Avoiding another Texas deep freeze

Posted: November 8, 2021

In February of this year, a statewide deep freeze occurred in Texas following a winter storm that rocked the property insurance industry. Significant damage resulted from a variety of issues following the storm. Most notably, the Texas power grid failed, leading to many uninhabitable homes in several heavily populated areas, including Houston and Dallas. Many people could not return to their homes for over two...

5 tips for separating work from personal life

Posted: November 3, 2021

Creating a clear separation between your work life and your personal life can be quite the challenge, especially if you’re working from home while in temporary housing. But without that separation, you’ll find yourself burnt out and unhappy. Here are some tips for how to create boundaries so you can have a more productive workday and experience greater enjoyment in your personal life. 1. Try...